Enter your email address to stay up to date on new releases

.png)

Subscriptions are ubiquitous nowadays. Instead of buying a single piece of quickly-outdated software for say, cash flow forecasting, we subscribe to a monthly SaaS product that promises to constantly update with changes in technology.

The same goes for digital products. Rather than going out and buying single pieces of media, we stream movies and shows on Netflix, or enjoy an all-you-can-read buffet of books with a subscription to Kindle Unlimited.

This is incredibly convenient for consumers. But for the sellers of these subscriptions? Some tax pitfalls are hidden in the increasingly popular subscription business model.

Are Subscriptions Taxable?

As with most US sales tax questions, it depends. US states make their own sales tax rules and laws, and sales tax on subscription varies by state according to factors like product type, whether it is “rented” or owned,” and even how the product is used by the end purchaser.

This article will help you determine if you should charge sales tax on your subscription-based business.

Defining subscriptions: SaaS vs. digital products

There are two basic categories when it comes to sales tax on subscriptions:

- Software as a Service (SaaS) - Subscription-based access to a software; it’s generally not downloaded to your computer, and your access to the product ends when you stop paying.

- Digital products - Digital downloads like songs, e-books, gaming, and movies are the common ones, but this can also include downloadables like educational cheat sheets or sewing patterns. The commonality is that these products are delivered to the buyer digitally rather than in tangible format.

For tax purposes, many states tax these items differently. For example, most states tax tangible personal property. So, they may consider the digital product (like an e-book) merely a digital replica of a tangible item, and thus consider it to have the same tax treatment as the tangible (and taxable) version of that item. This works both ways, if the item isn’t considered taxable then the digital replica generally isn’t considered taxable either.

On the other hand, the same state that taxes digital products might treat SaaS as a non-taxable service. Most states consider tangible items (like scarves or fruit bowls) taxable and services non-taxable. About half the states treat SaaS as a non-taxable service when it comes to taxability, especially when there is no tangible component (like a user’s manual), and no software is downloaded to your computer for you to keep once the subscription runs out.

This means that a state might tax a downloadable movie while not taxing a movie-streaming service like Hulu. Even though the consumer is basically getting the same product, the state is considering means of delivery rather than simply the nature of the product.

Why taxability varies so much

The short answer to why taxability varies so much that, in tax terms, digital products and subscriptions are relatively new concepts.

It takes time for states to realize that both a new way of selling goods and services has arrived, and to decide what to do about that. While some states have acted, others still haven’t made a specific law or letter ruling about the taxability of SaaS or digital goods, and instead rely on trying to fit subscriptions into existing legal frameworks.

And some states just define “what is a subscription?” or “what is a digital product?” differently than others.

As time goes on, taxability of certain goods and/or services generally harmonizes across states. That’s why, for example, groceries are not taxable in most states. But for now, we’re still in the Wild West where taxability of subscriptions varies greatly across states, and sometimes even within states.

Key Tax Concepts for Subscription Businesses

In the US, you often see the term “sales and use tax” (SUT) used. To understand taxability and who pays consumer taxes, it’s important to distinguish between these two interrelated but distinct concepts.

Sales tax vs. use tax

Sales tax is a tax on a transaction paid at the point of sale by the end-user. It’s collected by the seller and then periodically remitted back to the state. Businesses are required to collect sales tax when they meet certain physical presence or sales volume criteria in a state. (See “Nexus and thresholds” below).

Use tax is due when a buyer purchases an item for use in their state but the seller does not charge sales tax. Say a buyer in the sparsely populated state of Idaho buys a TV online, but the seller isn’t required to collect sales tax from buyers in Idaho. Instead, the buyer is required to pay the sales tax they would have paid on the TV.

This is generally part of a buyer’s state income tax filing. Many individual taxpayers are, understandably, unaware of this obligation. However, businesses fall under more scrutiny when it comes to keeping up with and remitting use tax, and never paying use tax can be a red flag to auditors that your business is not playing by the tax rules.

To sum it up, sales or use tax is due on every sales transaction, except in certain cases of very small one-off person-to-person transactions or where the buyer is buying the products with the intent to resell them.

Nexus and thresholds

Sales tax nexus is a legal connection between your business and a state that means you’re required to collect sales tax from your buyers in that state. Before the rise of digital commerce, nexus generally meant physical presence, such as having a location, employees, or inventory in a state.

But the 2018 South Dakota v. Wayfair Supreme Court ruling allowed states to also require businesses with “economic nexus” to collect sales tax from buyers in the state. Businesses who exceed a certain sales threshold (usually $100,000 and 200 transactions, but this varies by state) in a state are now required to collect sales tax from buyers in that state even if they have no physical ties to the state.

It’s important for SaaS and digital goods sellers to realize that even though you may operate out of a headquarters in one state, your sales volume could trigger sales tax nexus in a completely unexpected state – whether you have a physical presence there or not.

Get started

Solutions like Sphere , will automatically tell you if your state is approaching, or has already reached, a state’s nexus threshold.

Tax exemptions & certificates

In the US, purchases by the end user of an item (and, less often, a service) are taxable. As long as the item purchased was taxable, the buyer must pay either sales tax to the retailer or use tax directly to the state.

But purchases of goods to resale are generally not subject to sales tax. For example, a retailer who buys 1,000 lbs of fabric from their supplier and plans to turn that fabric into shirts to resell to the public isn’t required to pay sales tax on that fabric.

But it’s not as simple as telling your supplier you’re buying for resale. Retailers are required to present their supplier with a resale certificate (sometimes known as an “exemption certificate.”) This includes your name, business name and identifying information, your business’s sales tax ID (sometimes known as a “resale number”), and a description of the goods purchased and what they will be used for.

For wholesalers and other suppliers, this means validating that the sales tax ID/resale number you’ve been presented with is real (most states provide an online portal for this) and evaluating whether the items are being purchased in good faith.

For example, if your customer owns a toy store but is attempting to buy a hot tub from you tax free, there’s a fair chance that they aren’t truly buying that hot tub to sell it to clamoring parents on Black Friday. Don’t skip this step, because if a resale certificate turns out to be fake, the wholesaler/supplier is generally liable to pay the tax they didn't’ charge to their customer.

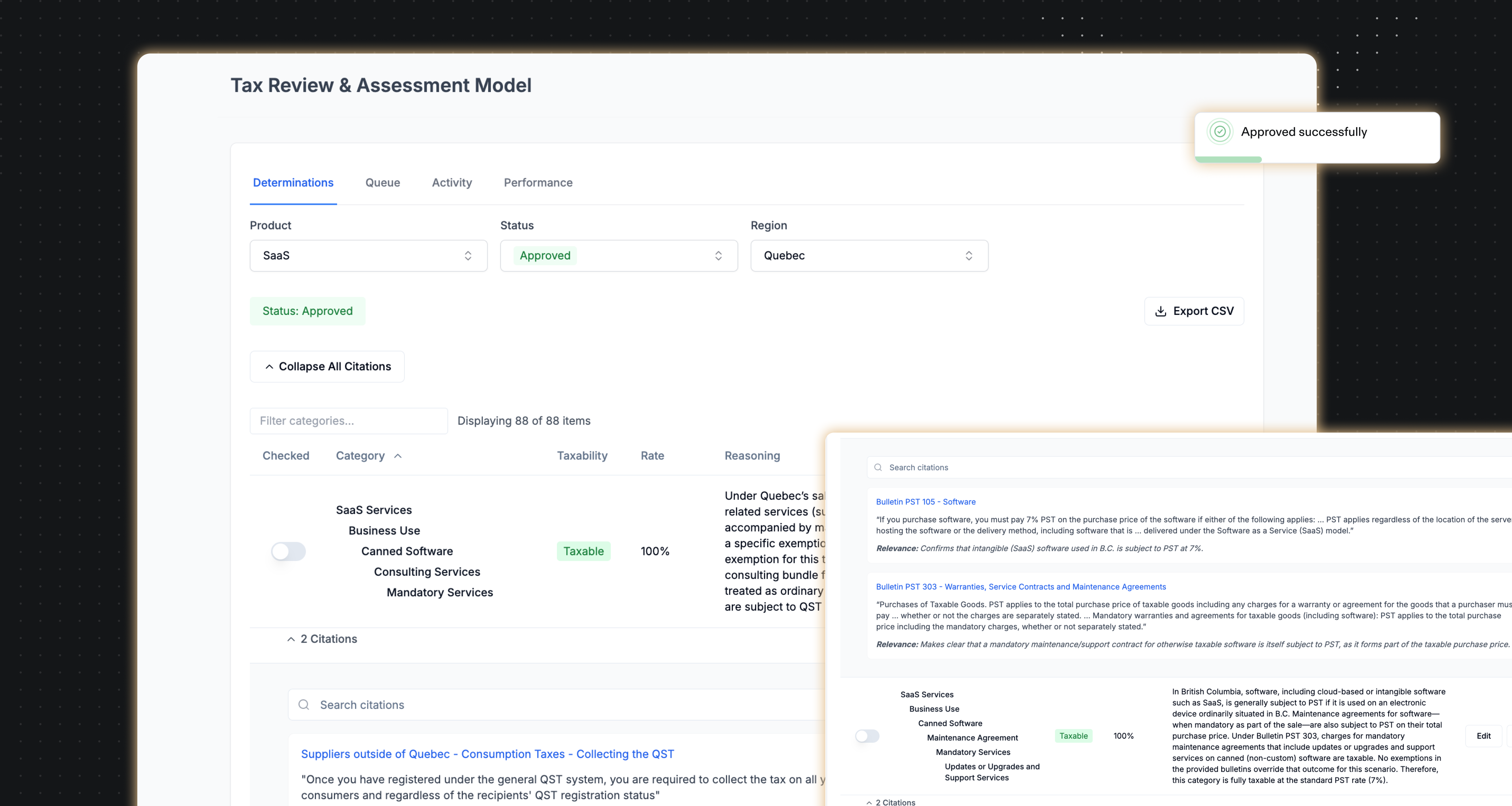

For subscription sellers, this means you must understand how your customer is going to use your product. For example, some states consider SaaS taxable for consumer use, but not for business use, and vice versa.

SaaS & Digital Subscription Taxability by State

Overview of the U.S. landscape

For the reasons we’ve already mentioned, SaaS and digital subscription taxability varies widely from US state to US state.

It should be further noted that sometimes digital products like a single downloaded movie with rights for permanent use are taxed by a state in one way while that same state taxes a streaming subscription (i.e. with rights of less than permanent use), such as Netflix, differently.

The below table explains subscription (and digital product) taxability in every US state.

Comparison table: State-by-state taxability

International Note

Subscriptions are generally taxable abroad

Whether they use VAT, GST, or another tax system, most countries treat digital products, including SaaS subscriptions and streaming subscriptions, as taxable. This tax treatment is common in the EU, UK, Canada, Australia, Japan, India and other countries.

B2B vs. B2C tax treatment

While, as a business, you are generally always required to collect VAT, GST, etc. on transactions, if you sell to other businesses you may not be required to collect. Many countries have what is called the “reverse charge mechanism” where the B2B buyer accounts for the tax.

This prevents you from having to register and collect indirect tax in a foreign country should you sell to other businesses. To comply, you must collect and verify your buyer’s tax ID to ensure that the reverse charge is applicable.

It’s always important to check each country’s tax laws to determine if the reverse charge mechanism applies to your B2B sales.

Non-resident sellers may still need to register

Many countries have a low or even no threshold when it comes to B2C sales. Evaluate before you begin making sales of your consumer-based SaaS or digital subscriptions into other countries.

How to Stay Compliant (and How Sphere Helps)

The compliance burden of managing it manually

With SaaS and digital subscription businesses, it's easier than ever to sell to customers in every US state and all around the world. But indirect tax traps can be waiting around the corner.

Making just 200 sales to buyers in Georgia can leave you liable to register and collect Georgia sales tax. Selling a digital subscription to a single customer in the United Arab Emirates can leave you on the hook for registering and collecting VAT from all of your UAE buyers.

Worse, tax liability can sneak up on you. You may not realize you have liability in a state or country until the penalties and interest are wracking up. This is especially true as tax laws update and change constantly.

How do you maintain the fun and profit of operating your subscription business without tearing out your hair over tax surprises?

How Sphere automates tax compliance for subscriptions

Trust Sphere. As the premier AI-powered sales and indirect tax solution for subscription businesses, Sphere takes all the guesswork out of tax compliance.

- Tax determination for complex subscription scenarios – Before, determining if your digital subscription is taxable in Ohio might have taken a team of researchers or an expert on retainer. Sphere’s AI-forward solution digests tax codes and helps you determine when you need to collect sales tax (or VAT, or GST…) and when you don’t.

- Automatic nexus tracking – How do you know when you get to $100,000 in sales or 200 transactions in Arkansas? Sure you could tally all this manually, but who has the time? Sphere has your back, letting you know when you’re approaching, or have already crossed, nexus thresholds so you can get registered and feel confident in your compliance.

- Streamlined filing and remittance (in the US and globally) – As your business grows, just filling out complex sales tax returns and getting them filed on-time with the state can become someone’s full time job. Unless you have Sphere. Automated remittance and filing both in the US and around the world saves your time and frees you up for more profitable activities.

- Exemption certificate management – Unfortunately, most states rely on you, as the business, to keep track of your buyer’s taxable status and even to assess and identify bad actors. Sphere helps you manage exemption certificates and can automatically validate VAT IDs to ensure you won’t run into trouble later.

With Sphere, you can finally take the mystery out of international tax compliance.

You Might Like

.png)

.png)

_%20Avoid%20Double%20Taxation%20%E2%80%93%20Complete%20Guide.png)

Make the world

one market

End-to-end compliance automation for sales tax, VAT, and GST. 100+ regions. One platform. Built by 50 people who believe the compliance cost of every transaction should be zero.