Enter your email address to stay up to date on new releases

Say your company buys $20,000 worth of equipment from an out-of-state vendor. The vendor doesn't charge you sales tax. You assume you're in the clear.

Except, that purchase probably triggers use tax. Use tax is a tax your company now owes directly to your state, even though no one collected any tax at checkout.

Sales tax and use tax are two sides of the same coin. Sellers collect sales tax. Buyers self-assess use tax when a seller doesn't charge them. Understanding the difference, and knowing when each tax applies, is essential for any business that buys or sells across state lines. Especially because auditors look for use tax discrepancies when going through your books.

This guide breaks down both taxes with real examples, explains how they differ from input tax, and shows what compliance actually looks like in practice.

The Quick Rule: Sales Tax vs Use Tax

Sales tax is collected by the seller at the point of sale. Use tax is paid by the buyer when sales tax wasn't charged.

These two taxes work together. If a seller collects sales tax on a transaction, the buyer generally doesn't owe use tax on that same purchase. But if no sales tax was collected the buyer may owe use tax instead.

Both taxes typically apply to the same types of goods and services. They just put the compliance responsibility on different parties.

Sales Tax in Practice: When Businesses Must Collect It

What is sales tax?

Sales tax is a percentage-based tax on retail sales of tangible personal property and certain taxable services. The seller collects it from the buyer at checkout and then remits it to the state.

Here's a simple example: A hardware store in Nashville, Tennessee, sells a drill press for $500. Tennessee's combined state and local sales tax rate is around 9.75%. The store charges the customer $548.75 — $500 for the drill press plus $48.75 in sales tax. The store then sends that $48.75 to the Tennessee Department of Revenue.

When must businesses charge sales tax?

Businesses must collect sales tax when they have "nexus" (aka a legal connection) in a state.

There are two main types of nexus:

- Physical nexus means your business has a presence in the state. That includes offices, warehouses, employees, or even a home office.

- Economic nexus means your business has crossed a sales threshold in the state, even without a physical presence. Most states set this at $100,000 in annual sales or 200 transactions. This rule came out of the 2018 Supreme Court decision in South Dakota v. Wayfair.

Once you have nexus in a state, you must register for a sales tax permit, collect sales tax from buyers in that state, and remit it to the state's department of revenue.

Filing and Remitting Sales Tax

After collecting sales tax, sellers file a sales tax return. They generally file monthly, quarterly, or annually, depending on sales volume. The return breaks down how much tax was collected by state, county, city, and special taxing district. Then the business remits the collected amount to the relevant tax authority.

Missing a filing deadline or remitting the wrong amount can result in penalties, so tracking collection by jurisdiction matters.

Use Tax in Practice: When Buyers Must Self-Assess Tax

What is use tax?

Use tax is a self-assessed tax on taxable goods or services that were used, stored, or consumed in a state when sales tax was never charged on that purchase.

Use tax exists to level the playing field. Without it, businesses could simply buy everything from out-of-state vendors to avoid ever paying sales tax.

Here's an example: A marketing agency in Virginia orders $5,000 worth of office furniture from a vendor in Oregon. The Oregon vendor has no nexus in Virginia and doesn't charge Virginia sales tax. The agency now owes Virginia use tax on that $5,000 purchase. According to the Virginia Department of Taxation, businesses must self-report and pay this tax directly to the state.

Common Use Tax Scenarios

Use tax tends to catch businesses off guard. Here are the situations where it comes up most often:

- Out-of-state purchases. Buying from a vendor that has no nexus in your state and doesn't charge you sales tax.

- Online orders. Purchasing through an e-commerce platform from a seller that isn't registered in your state.

- Items bought for resale, then used internally. A retailer buys inventory tax-free using a resale certificate, then pulls some items off the shelf for internal use. Use tax is owed on those items that weren’t resold.

- Software and digital subscriptions. A company in a state where SaaS is taxable subscribes to a platform whose vendor doesn't charge sales tax. Use tax applies here.

- Trade show or conference purchases. A company buys equipment at an event in another state, ships it home, and the vendor doesn't charge the home state's sales tax.

How Businesses Report Use Tax

Businesses report use tax on a use tax return or on their regular sales tax return, depending on the state. They calculate the tax themselves based on the purchase price and the applicable state or local tax rate. Then they remit the amount owed directly to the state tax authority.

The District of Columbia, for example, requires businesses to file a combined sales and use tax return and report both taxes in the same filing. Many other states follow a similar model.

The challenge is that use tax has no automatic collection mechanism. Businesses must track every out-of-state or untaxed purchase on their own — which is where a lot of companies fall short.

Similarities Between Sales Tax and Use Tax

Sales and use tax are complementary taxes. Here’s how that works.

They Apply to the Same Tax Base

Sales tax and use tax generally apply to the same types of transactions: taxable goods and certain taxable services. The rate is usually the same too. If a state has a 6% sales tax, the use tax rate is typically 6% as well.

They Fund the Same Government

Both taxes flow to the same destination: the state's taxing authority. States use both to fund services like roads, schools, and public health programs. The two taxes work together so the state doesn't miss out on revenue just because a purchase happened across a border.

They are Administered by the Same Tax Authorities

Sales tax and use tax fall under the same tax compliance ecosystem. Both are managed by the same state and local taxing jurisdictions. Both require registration, recordkeeping, and periodic reporting to the same state revenue agencies.

Key Differences Between Sales Tax and Use Tax

Who Pays and Who Remits

Sales tax is collected by the seller from the buyer at the point of sale. The seller is legally responsible for remitting that tax to the state.

Use tax is self-assessed by the buyer. There's no seller in the picture collecting it. The buyer has to calculate what they owe and remit it themselves. This is where the compliance burden shifts entirely to the purchasing business.

When Each Tax Applies

Sales tax applies at the moment of purchase. It's charged on the invoice, collected at checkout, and remitted at the end of the filing period.

Use tax applies after the fact. When a business realizes it received taxable goods without being charged sales tax, they must remit use tax. The obligation kicks in when the goods are first used, stored, or consumed in the state.

What Compliance Looks Like in Practice

For sellers, sales tax compliance means registering in nexus states, setting up tax collection on invoices, and filing returns on time.

For buyers, use tax compliance means reviewing purchase records, identifying transactions where sales tax wasn't charged, calculating the amount owed, and self-reporting it. Many businesses track this through an internal use tax accounting process.

The operational difference is significant. Sellers have systems to automate collection. Buyers often track use tax manually. And this increases the risk of errors and missed obligations.

Use Tax vs Input Tax (A Common Global Tax Confusion)

What is input tax?

Input tax is the VAT or GST a business pays on its own purchases and expenses. In most VAT/GST systems a registered business can deduct the input tax it paid from the output tax it collected from customers.

For example, a UK retailer pays £200 in VAT on a supplier invoice. That £200 is input tax. If the retailer collected £800 in VAT from its own customers that quarter, it remits only £600 to HMRC. That’s the £800 collected minus the £200 input tax credit.

Input tax reduces what a business owes in taxes.

How Use Tax Differs from Input Tax

Use tax works in the opposite direction. There's no credit or deduction mechanism. If a business in Ohio owes use tax on a $10,000 software purchase, it pays that amount directly to the Ohio Department of Taxation. It gets nothing back.

Use tax increases a business's tax bill. Input tax reduces it.

This is a common point of confusion for finance teams at companies operating in both the US and international markets. The taxes are not the same, they don't work the same way, and treating one like the other creates compliance problems.

How to Stay Compliant With Sales and Use Tax

Track Taxable Purchases

The first step is knowing what you bought and whether sales tax was charged. Review vendor invoices regularly and flag any purchase where sales tax is missing. Not every untaxed purchase triggers use tax, but many do. Set up an internal process to capture these transactions before they become a problem at audit time.

Monitor Nexus and Rate Changes

Economic nexus thresholds and state tax rates change. A business that didn't have nexus in a state last year may have it now based on sales growth. State legislatures also pass new sales tax laws regularly. For example, Kentucky began taxing SaaS on January 1, 2023, and Vermont followed suit on July 1, 2024.

Staying on top of nexus changes and rate updates is an ongoing responsibility.

Maintain Proper Documentation

Keep resale certificates, exemption certificates, and purchase records organized and accessible. If a state audits your business, documentation is your primary defense.

For use tax specifically, maintain a log of out-of-state and untaxed purchases. States can and do audit use tax compliance. The California State Board of Equalization, the Texas Comptroller, and the New York Department of Taxation and Finance have all historically been active in this area.

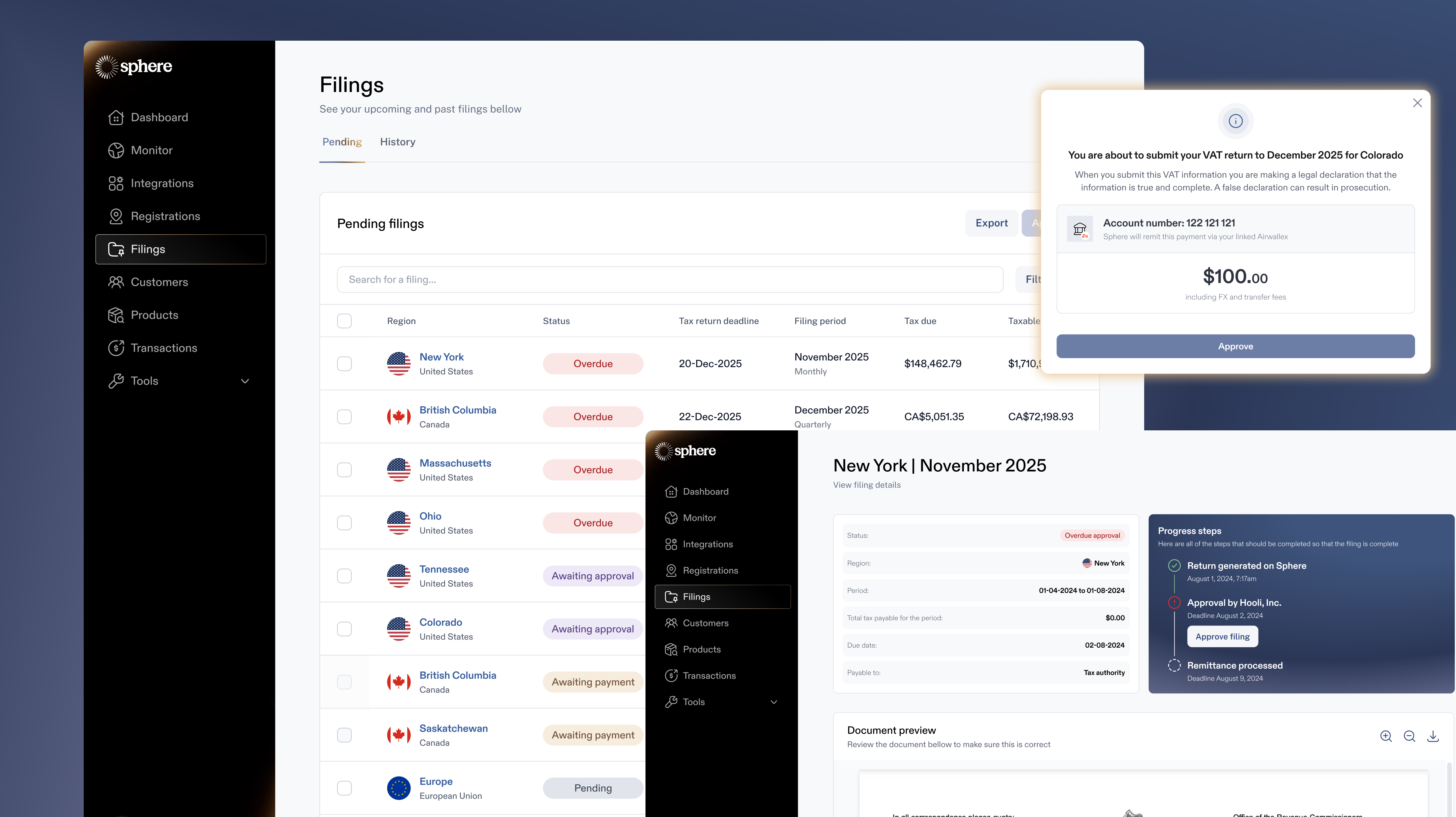

How Sphere Automates Sales and Use Tax Compliance

Managing sales and use tax manually is a real risk for growing companies. Here's how Sphere handles it.

Automated Monitoring and Registration

.png)

Sphere continuously monitors your sales activity across every US state and international jurisdiction. When your business approaches an economic nexus threshold, Sphere alerts you. Sphere then manages the registration process with the relevant tax authority so you don't miss your compliance window.

Automated Tax Calculation

Sphere's AI-powered tax engine calculates the correct sales tax or use tax at the point of transaction. It accounts for state and local rates, product taxability rules, and exemption certificates. The right amount is applied every time, without manual lookups.

Automated Filing and Remittance

Sphere handles the filing and payment side too. Returns are prepared, validated, and submitted to state revenue agencies automatically. That includes both seller-side sales tax filings and buyer-side use tax remittances.

For companies operating internationally, Sphere's platform covers VAT and GST as well, including input tax treatment in relevant jurisdictions. It's one platform for all indirect tax compliance, domestic and global.

Get started

Solutions like Sphere , will automatically tell you if your state is approaching, or has already reached, a state’s nexus threshold.

The Bottom Line: If Sales Tax Isn’t Collected, Use Tax Still Exists

Sales tax is collected by the seller. Use tax is self-assessed by the buyer when the seller didn't collect. Both taxes apply to the same types of transactions. Both create compliance risk if your team isn't tracking them closely.

The difference that catches most businesses off guard: use tax has no automatic collection mechanism. It's on you to find the gap and report it. That's exactly the kind of task that falls through the cracks in fast-growing companies with lean finance teams.

Automation is the practical fix. Sphere monitors your transactions, calculates what you owe, and files on your behalf. With Sphere, neither sales tax nor use tax becomes a liability you discover at audit time.

You Might Like

.png)

Make the world

one market

End-to-end compliance automation for sales tax, VAT, and GST. 100+ regions. One platform. Built by 50 people who believe the compliance cost of every transaction should be zero.