Enter your email address to stay up to date on new releases

Businesses with complicated tax footprints are increasingly being audited. And it’s not always about wrongdoing. Sales tax compliance has become incredibly complex, with economic nexus laws creating tax obligations in new states, varying sales tax rules from state to state, and the complexity of taxing SaaS and digital products.

Small errors like repeated late filings, having exempt sales, failing to report use tax, or even simply high transaction volumes can put you on an auditor’s radar. Plus, states are now relying on data monitoring to flag audit risk, so your business might simply run afoul of an algorithm without a human auditor ever clicking through your account.

This guide shows you exactly what triggers audits, what the process looks like, and how modern finance teams stay audit-ready.

Why Are More Businesses Getting Audited Now?

Sales tax audit rates have surged because states need the revenue, and they now have better, data-driven ways to target noncompliant businesses.

Data Triggers & Red Flags

States are now using AI and machine learning to spot audit targets by cross-referencing multiple data sources. For example, if you file both sales and income tax in a state and those totals don’t match, that’s a big red flag. Other factors like repeated late filings, incorrect tax calculations, a large number of exemptions, or failure to report use tax due also get an auditor’s attention.

Nexus Expansion & Multi-State Risk

The 2018 Wayfair v. South Dakota Supreme Court decision opened the door for states to require sales tax from more businesses than ever. While before a business had to have some sort of physical presence in the state to be on the hook for sales tax, now e-commerce and digital businesses are required to collect sales tax based on transactions and revenue. Most states set their thresholds at around $100,000 in sales or 200 transactions annually.

This has made sales tax management for digital and e-commerce brands an everchanging puzzle. It’s easy to cross nexus thresholds in a new state without realizing it. And failure to collect sales tax in states where your business has economic nexus invites scrutiny and audits.

States use data from payment processors, marketplace facilitators, and information-sharing agreements to find businesses that should be registered but aren't. Once they find you, they'll assess back taxes for 3-4 years, plus interest and penalties.

Industry Hotspots

Certain industries face higher audit scrutiny due to complex taxability rules and high transaction volumes. SaaS and digital companies make that list because their products are taxable in some states, exempt in others, and partially taxable in a few more.

E-commerce businesses face multi-state compliance challenges that create frequent audit exposure. Manufacturing companies have trouble managing exemption certificates for wholesale sales. All three industries show recurring audit findings in state reports.

Other high-risk industries are construction, healthcare, and professional services. Construction has mixed taxable and exempt sales. Healthcare often has exempt sales to nonprofits and government groups. Professional services have complex sourcing rules.

Inside the Sales Tax Audit Process

Understanding what happens during a sales tax audit helps you prepare and respond effectively. The process is similar across most states.

Notification & Scope

The audit process is initiated with a notification letter from the state’s taxing authority (usually called the department of revenue). The letter identifies your business as the audit subject, names your assigned auditor, and specifies the lookback period, which is usually 3 or 4 years.

The letter also defines the scope. Most audits cover sales tax collection and remittance, but the department of revenue might also review use tax compliance, exemption certificate validity, and local tax reporting (such as Chicago’s amusement tax). Some audits target specific issues like exempt sales.

Common triggers that lead to audits of prior tax returns include discrepancies in reported sales, late filings, economic nexus violations, or industry-wide audit initiatives. Use tax audits often stem from large capital purchases showing up on depreciation schedules without corresponding use tax payments.

You typically have 10-30 days to acknowledge the audit and begin gathering documents. Don't ignore this letter. Non-response can lead to default assessments based on the state's estimates rather than your actual records.

Document Requests

Auditors will request extensive documentation. The initial document request usually includes:

- All sales tax returns for the audit period

- Use tax returns and accrual records

- Purchase invoices, especially for capital expenditures

- Resale certificates from wholesale customers

- Exemption certificates from tax-exempt buyers

- General ledger and trial balance

- Sales journals and detailed transaction records

- Federal and state income tax returns

- Bank statements and credit card processor reports

Having tax reporting organized across jurisdictions is critical. If you operate in multiple states, auditors want to see how you allocated sales, tracked nexus, and calculated tax obligations for each jurisdiction.

Missing or disorganized records slow the audit process and increase the likelihood of adverse findings. Auditors may estimate tax due based on incomplete information, which usually results in higher assessments than your actual liability.

Examination & Findings

Auditors test transactions to verify you collected the correct tax, validated exemptions properly, and reported accurately. Auditors usually check a sample period, often one quarter, in detail. Then they estimate error rates for all sales during the audit period.

The examination focuses on:

- Sales transactions to verify proper tax collection

- Exemption certificates to confirm completeness and validity

- Purchases to identify missing use tax payments

- Tax return calculations and jurisdiction allocations

- Sourcing rules and product taxability determinations

Auditors check exemption certificates to make sure they have the business name, address, tax ID, reason for exemption, signature, and date. A certificate missing any required field invalidates the exemption.

Missing documentation often leads to assessments—even if sales were truly exempt. If you claimed an exemption but can't produce a valid certificate, the auditor will assess tax, interest, and penalties on that transaction. This is why ironclad documentation is your primary defense.

When auditors find errors in the sample period, they extrapolate those findings. If 5% of your sampled transactions lacked proper documentation, they'll apply that 5% error rate to your entire sales volume for the audit period.

Final Assessment or Dispute

The audit concludes with the auditor's findings. If no issues were found, you receive a "no change" letter closing the audit. More commonly, the auditor issues an assessment for additional tax due, plus interest and penalties.

The assessment breaks down:

- Base tax you should have collected but didn't

- Interest calculated from the original due date of each tax period

- Penalties for late payment, negligence, or fraud

Interest rates vary by state but typically range from 3-10% annually. Penalties usually range from 5-25% of the tax due, depending on whether the state views errors as innocent mistakes or willful non-compliance.

You have options if you disagree with the assessment. Most states allow you to request a supervisor review, provide additional documentation, or file a formal appeal. Working with a CPA or tax attorney can help you navigate dispute procedures and negotiate settlements.

Many states will waive penalties if you can demonstrate good faith compliance efforts or if this is your first audit. Interest waivers are rare but sometimes available in cases of state error.

In rare cases, overpayments present an opportunity to recover taxes. If the audit reveals you've been overpaying sales tax, you can request a refund or tax credit for past periods. However, refund claims are usually limited to 3-4 years from the original payment date.

8 Audit Triggers You Can’t Ignore

These specific issues leave you open to audit. Put sales tax compliance processes in place now to spare the pain of an audit later.

Exempt Sales Without Proper Certificates

When selling products or services that are normally taxable without charging the tax, you must prove that the transaction was legitimate. This means complete exemption certifications with all required fields filled in.

States require exemption certificates to have the business name, address, tax ID number, reason for exemption, signature, and date. Some states have additional requirements like expiration dates or specific certificate forms.

Even if the transaction was legitimately tax-free, if you fail to provide the documentation you’ll be on the hook for paying the uncollected tax. For example, a single missing signature on a $100,000 sale could cost you $8,000-$10,000 in tax, interest, and penalties.

Unregistered States with Economic Nexus

It’s easy for technology companies to trigger economic nexus without realizing it. If you’re not breaking down your sales by state, you may not realize you’ve hit Colorado’s $100,000 transactions or California’s $500,000 threshold.

Failing to comply can lead to a retroactive audit. States can assess back to when you first had a nexus obligation. Those taxes you unknowingly failed to collect, plus interest, can add up fast.

Inconsistent Sales Reporting

Mismatches between sales tax returns, other state tax, income tax filings, and general ledger entries trigger automated flags. Your income tax return shows $1 million in revenue, but your sales tax returns only report $600,000 in sales across all states. Where's the other $400,000?

The difference might be exempt sales, out-of-state sales, or services. But without clear documentation explaining the gap, auditors assume you underreported taxable sales.

Monthly reconciliation catches these errors early. Compare your sales tax reports to your financial statements every month. Document any differences with clear explanations tied to specific transactions.

Large Capital Purchases Without Use tax

Use tax is the companion to sales tax. When you buy equipment, software, or other taxable items from out-of-state vendors who don't charge your state's sales tax, you owe use tax.

Auditors check this by comparing depreciation schedules to use tax returns. That $50,000 in fixed assets showing up on your balance sheet? If there's no sales tax paid and no use tax reported, that's a red flag.

Missing use tax payments are audit gold for states. Most businesses don't even know use tax exists, creating an easy revenue source for departments of revenue.

Filing Gaps or Late Payments

Missing or late tax payments increase attract auditors’ attention. States track compliance patterns. A pattern that shows repeated late or missed filings may have the auditor asking what else is wrong in your business.

The audit period scope may widen based on poor filing history. If you have multiple late payments or missed filings, auditors might extend their review beyond the standard 3-4 years or conduct more detailed examinations.

Prior Audit Activity

A customer's audit can lead to a vendor audit. When states audit your customers and find improperly documented exempt purchases, they'll contact you to verify the exemption certificates. If you can't produce valid certificates, you're now also on the audit list.

Vendor audits trace back to your company through supply chain reviews. States might audit manufacturers, find issues with their wholesale purchases, then audit their suppliers to verify resale certificates.

This cascade effect means one audit can trigger five more across your customer and supplier base.

High Refund or Credit Claims

Large refund requests for additional tax or overpayments get flagged for review. States scrutinize refund claims because they represent money going out instead of coming in.

Refund requests over $10,000 almost always trigger examination. Multiple refund requests in a short period raise additional suspicion. States want to verify you actually overpaid and aren't gaming the system.

Operating in High-Risk States

States with well-funded taxing authorities like California, New York, and Texas audit more frequently than others. Pay close attention if you have sales tax nexus in these aggressive states.

To compound matters, these states all have complex state and local rates and rules. California has over 500 local tax jurisdictions. New York has dozens of special taxing districts.Texas taxes SaaS in a unique way. Getting the details right across all these jurisdictions is challenging, creating more opportunities for errors.

How to Prepare for a Sales Tax Audit

The best audit defense is organized sales tax compliance before the dreaded audit letter arrives. This proactive checklist helps you get audit-ready today.

Build an Audit-Ready Record System

Create a digital filing system that includes all the documentation your auditor will want to see, including:

- Sales tax returns by period and jurisdiction

- Use tax calculations and payments

- Exemption certificates and resale certificates organized by customer

- Purchase invoices for all capital expenditures

- General ledger reconciliations

- Supporting documentation for any unusual transactions

Digitize and regularly review resale certificates and exemption certificates. Check for missing signatures, expired dates, or incomplete information. Contact customers to update invalid certificates before an audit finds them.

Review purchase invoices quarterly to identify items that might need use tax payments. Pay special attention to out-of-state purchases over $1,000, because auditors definitely will.

Review Filing Accuracy

Check for discrepancies between your sales tax returns, general ledger, and tax reporting platforms. These mismatches are the number one audit trigger.

To review:

- Compare total sales on tax returns to revenue in your general ledger

- Verify exempt sales are properly documented

- Check that tax rates match current rates for each jurisdiction

- Confirm nexus determinations are still accurate

- Reconcile payments to filed returns

Review the taxability rules every quarter. Product taxability rules change, and new precedents emerge. What was exempt last year might be taxable now.

Review thresholds and tax rates regularly. Economic nexus thresholds vary by state. Some states count all sales, others only retail sales. Stay current on these rules to avoid surprise sales tax nexus in a new state.

Validate Use Tax Payments

Audit your capital purchases, especially equipment and software from out-of-state vendors. These are the most common source of use tax discrepancies.

For each capital purchase:

- Check if sales tax was paid at purchase

- If not, verify use tax was accrued and paid

- Confirm the correct tax rate was used

Out-of-state vendor purchases need special attention. If the vendor didn't charge your state's sales tax, you owe use tax. This includes cloud software subscriptions, equipment purchases, and professional services in some states.

Remit missing use tax before auditors flag it. Voluntary compliance demonstrates good faith and may help reduce penalties if issues are found in other areas.

Assign a Point Person

Designate a finance lead or external tax professional (CPA or specialized sales tax accountant) to interface with the auditor. This person becomes your single point of contact for all audit communications.

Your point person should:

- Understand your tax processes and systems

- Have authority to access and provide documents

- Know when to escalate issues to legal counsel

- Maintain detailed notes of all auditor interactions

Keep communication in one place to avoid conflicting answers or problems delivering documents. If multiple people talk to the auditor, you risk inconsistent explanations that create suspicion.

Consider hiring external help even if you have internal tax expertise. Sales tax audits are specialized, and tax professionals who handle them regularly know what auditors look for and how to present your case effectively.

Conduct a Dry Run Audit

Partner with a tax advisor to simulate an audit before the real thing happens. This exercise reveals weaknesses while you can still fix them without penalties.

The dry run process:

- Pull all documents an auditor would request

- Review a sample period in detail

- Test your exemption certificate files

- Calculate potential exposure for any issues found

- Fix problems and update procedures

Use this to uncover missing records, outdated rates, or overreported income. Better to find these issues yourself than have an auditor discover them.

Document your findings and remediation steps. If a future audit finds similar issues, you can demonstrate you took corrective action when you discovered the problem.

Automate Compliance Before an Auditor Knocks

Manual systems can't scale across states. Here's how Sphere helps automate audit-readiness so you can focus on growing your business instead of managing sales tax compliance.

Real-Time Nexus Monitoring

.png)

Sphere alerts you when you cross economic nexus thresholds, tracking sales and transactions across all states automatically. You'll know exactly when you've hit $100,000 in sales to Pennsylvania customers or 200 transactions in Ohio.

This prevents non-compliance by ensuring timely registration and collection. No more surprise nexus discoveries during audits. No more retroactive assessments for states you didn't know you should be registered in.

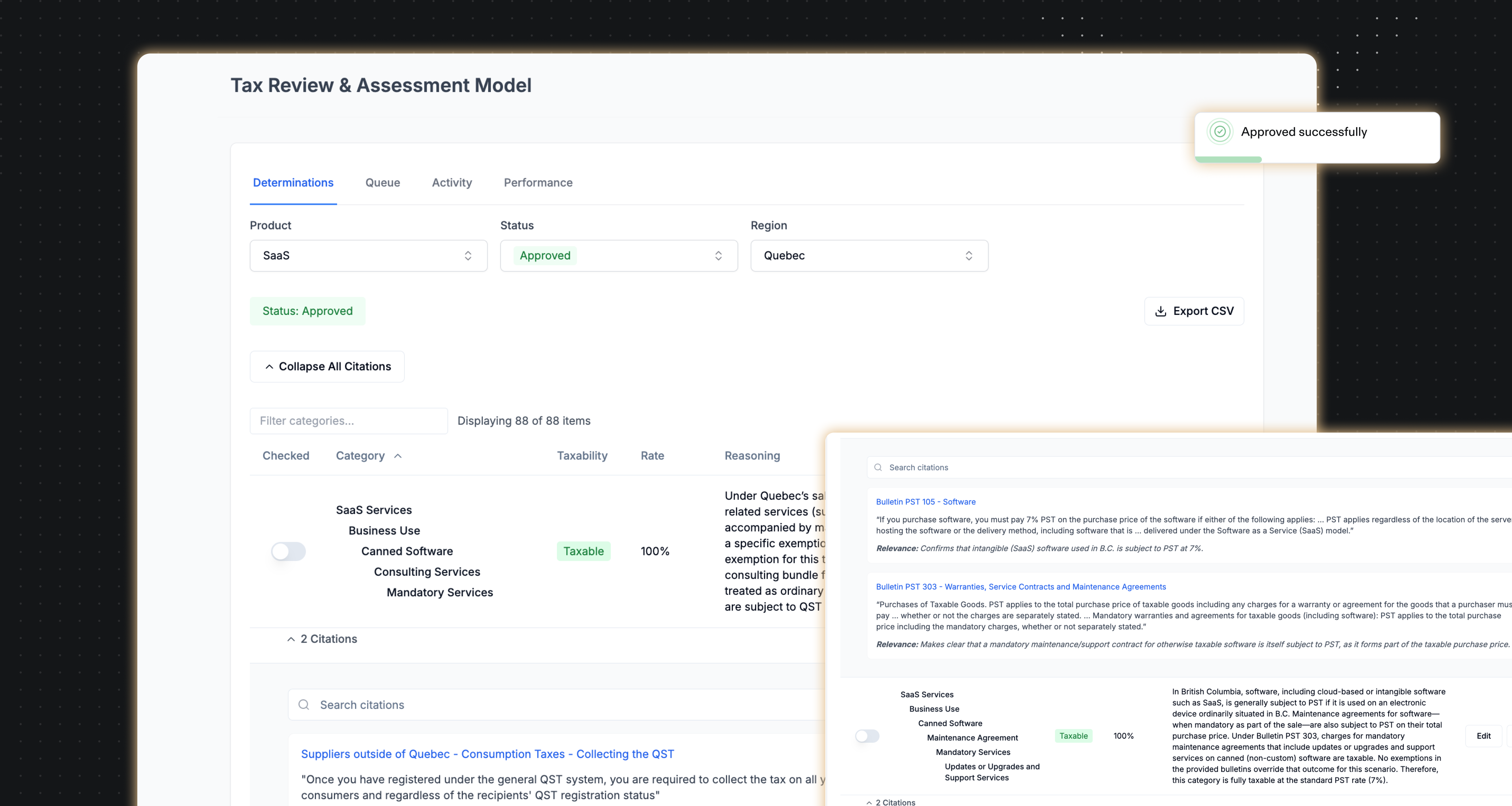

Sales Tax Calculation Accuracy

Sphere automates tax rates, sourcing logic, and product taxability, eliminating the calculation errors that trigger audits. The platform knows that your SaaS product is taxable in Arizona but not in Arkansas, and that clothing under $110 is tax-exempt in New York but fully taxable in Florida.

Accurate calculations lower manual errors and mistakes that trigger audits. No more applying 7% when the rate is actually 7.375%. No more forgetting special district taxes. No more accidentally charging tax on exempt products.

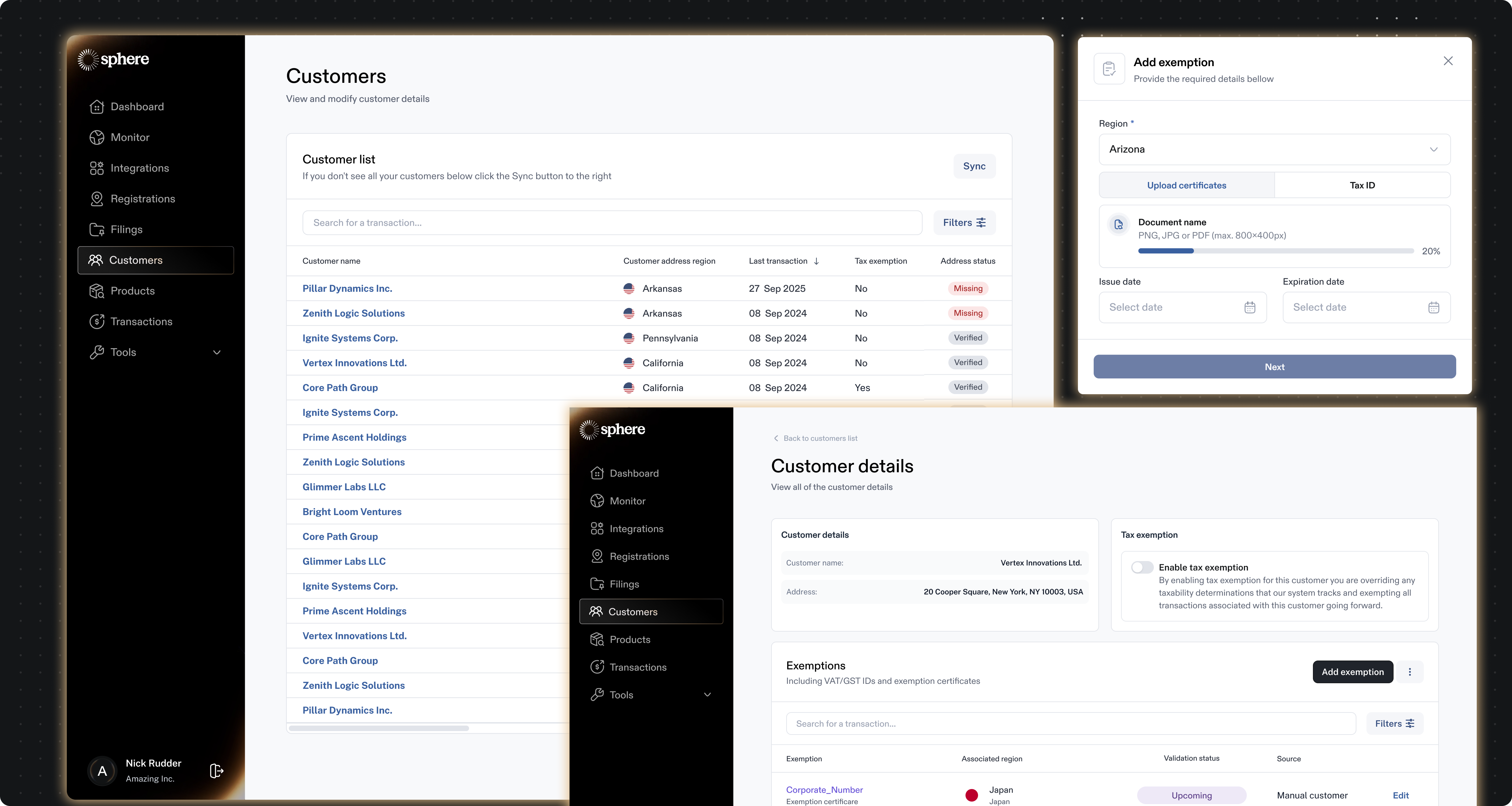

Exemption Certificate Management

Lost or invalid certificates are the number one cause of adverse audit findings. Sphere centralizes and automates collection and storage of resale certificates and exempt sales documentation. No more struggling to find your most up-to-date exemption certification information while the auditor waits.

Filing, Reporting, and Documentation

.png)

Sphere handles sales tax returns, use tax returns, and payment tracking across all jurisdictions. The platform prepares returns using your actual transaction data, not estimates or manual calculations. This digital audit-trail is built automatically as part of your normal business activities. It means you can quickly and easily assemble all the documentation your auditor requires.

Expert Support for Complex Tax Rules and Laws

Sphere's tax engine is built by experts who understand sales tax laws, edge cases, and jurisdictional quirks. Tax rules change constantly, with states making new product taxability determinations while local areas change up their rates.

Your team gets the peace of mind of having tax experts at your back.

When You’re Always Audit-Ready, You’re Always in Control

Audits aren't always random. Increasingly, they're targeted, data-driven, and aggressive. States now have sophisticated technology and revenue targets to hit. Using algorithms, they know which businesses are likely to have issues before they start the audit.

Finance leaders who rely on spreadsheets or outdated tools are left exposed. Manual processes can't keep up with economic nexus in 46 states (and DC), changing tax rates, complex product taxability, and mountains of exemption certificates.

The companies that thrive in this environment automate before problems arise. They track nexus in real-time, maintain perfect documentation, and can respond to any audit request within hours instead of weeks.

With Sphere’s automated compliance eliminates the triggers that put businesses on audit lists in the first place. When audits do happen, you're ready with organized records, accurate calculations, and expert support.

Audits are expensive, disruptive, and stressful. But they don't have to be. Build audit-readiness into your daily operations instead of scrambling when the letter arrives.

You Might Like

.png)

Make the world

one market

End-to-end compliance automation for sales tax, VAT, and GST. 100+ regions. One platform. Built by 50 people who believe the compliance cost of every transaction should be zero.