Enter your email address to stay up to date on new releases

Canada’s Digital Services Tax (DST) passed but was then put on pause. It now hangs in limbo until Parliament formally repeals it. Because the tax is technically in effect right now, business leaders need to understand Canada’s DST thresholds, sourcing rules, and how to comply.

This guide cuts through the confusion to explain what DST is, who it affects, how it’s calculated, and what your finance team should do next. DST is just one example of global tax uncertainty, and highlights why automated, AI-powered tax compliance is now essential for businesses making global sales.

What Is Canada’s Digital Services Tax (DST)?

Canada’s Digital Services Tax is a 3% tax on certain digital services revenue earned from Canadian users. The tax targets large, digital-first platforms–both Canadian and foreign companies–that generate significant revenue from Canadian users through online marketplaces, digital advertising, social media services, or user data sales.

DST doesn’t replace GST/HST or corporate income tax. It’s an additional tax that applies to gross revenue, not profits, meaning even unprofitable companies can owe DST if they exceed the revenue thresholds. Canada designed this tax as an interim measure while waiting for international consensus on digital taxation through the OECD.

Parliament passed the Digital Services Tax Act in June 2024, but it applies retroactively from January 1, 2022. This means some companies could face multiple years of DST obligations when or if collection resumes.

Canada's DST timeline reveals the political complexity:

- 2020: Canada first proposes DST as part of broader tax reform

- June 2024: Parliament passes DST legislation with retroactive application to January 1, 2022

- June 2025: Government announces pause on DST collection following US trade pressure

- Late 2025: DST remains legally active pending formal repeal legislation

This uncertainty makes planning nearly impossible. While over 40 countries worldwide have implemented similar digital services taxes, Canada's version stands out for its on-again, off-again status that leaves businesses guessing about their obligations.

Current Status: Rescinded but Not Repealed

Government Pause and Trade Pressure

The US government argued that Canada’s DST unfairly targeted American tech companies. Under this trade pressure, Canada agreed to pause DST collection in June 2025. Collection deadlines were immediately canceled, and the Canada Revenue Agency (CRA) suspended all DST filing obligations for the 2025 tax year.

Confusingly, this pause came just days before the first DST returns were due on June 30, 2025, leaving many businesses scrambling to understand their obligations.

CRA Guidance and Refund Path

The Canada Revenue Agency (CRA) has confirmed that no DST returns are required for 2025. Companies that had already registered or made advance payments should expect refunds, though the timeline remains unclear.

According to the CRA's latest guidance, businesses should maintain their DST registrations but take no further action until Parliament passes repeal legislation. The agency has committed to providing at least 60 days' notice before any new filing requirements take effect.

Companies should check the CRA’s official DST page for the most up-to-date guidance.

Legal Status in Late 2025

The Digital Services Tax Act (DSTA) continues to exist in Canadian law. It remains legally in force until Parliament formally repeals it, creating uncertainty for businesses trying to plan for 2026 and beyond.

While repeal legislation is expected, Parliamentary delays could leave DST in legal limbo for months. Finance teams should monitor developments closely, especially if your business approaches the revenue thresholds that will require compliance.

Some companies may still need to recognize potential DST exposure in financial statements, even with collection paused. Public companies or those seeking investment should pay particular attention to DST exposure.

Who Is Liable for DST?

Global Revenue Thresholds

DST applies only to large digital businesses that meet both of these thresholds:

- Global revenue of C$750 million or more in the previous calendar year

- Canadian-sourced digital revenue exceeding C$20 million in the calendar year

Both thresholds must be met for DST to apply. This means smaller companies and most startups won't face DST obligations, but fast-growing platforms need to monitor their trajectory carefully.

The global revenue threshold uses the same €750 million mark as many other international tax rules, including the OECD's Pillar One proposals. If your business already tracks this threshold for other jurisdictions, you're halfway there.

In-Scope Revenue Types

DST applies to four specific categories of digital services revenue:

- Online marketplaces: Revenue from connecting buyers and sellers, including transaction fees, subscription fees, and premium placement charges

- Online advertising: Revenue from displaying targeted ads to users, including programmatic advertising and sponsored content

- Social media platforms: Revenue from providing social interaction platforms, including premium subscriptions and business tools

- Sale or licensing of user data: Revenue from selling or licensing data collected from users of your digital services

SaaS subscriptions that don't fall into these categories generally aren't subject to DST. However, if your platform includes marketplace features, advertising components, or data licensing, those revenue streams might trigger DST obligations.

Canadian User Sourcing

DST applies when making sales to Canadian users. Revenue counts as "Canadian-sourced" based on the user’s location, not where your business operates. The CRA uses several factors to determine user location:

- IP address at time of interaction

- Billing address for paid services

- User-provided location information

- Device location data (for mobile apps)

Different rules apply to each revenue type. For marketplace revenue, if either the buyer or seller is in Canada, 50% of the transaction counts as Canadian-sourced. For advertising, 100% counts if the ad viewer is in Canada. These attribution rules can get complex quickly, especially for global platforms.

How Is DST Calculated?

Tax Rate and Deduction

The DST rate is straightforward: 3% on in-scope Canadian revenue exceeding C$20 million. The first C$20 million serves as a deduction, meaning smaller digital businesses making less than that amount do not have to comply.

For corporate groups, the C$20 million deduction must be allocated across all group entities with Canadian digital revenue. You can't claim the full deduction for each subsidiary. Instead, it's one deduction per corporate group, prorated based on each entity's share of Canadian revenue.

This gross revenue tax means profitability doesn't matter. Even if your Canadian operations lose money, you still owe DST if you exceed the thresholds.

Allocation by Revenue Type

Each revenue category has specific sourcing rules:

- Marketplace transactions: 50% attributed to Canada if one party (buyer or seller) is Canadian; 100% if both are Canadian

- Digital advertising: 100% attributed if displayed to Canadian users; 0% if displayed elsewhere

- Social media services: Based on user location when accessing the platform

- Data sales: Based on the location of users whose data is included in the dataset

These rules mean you need detailed tracking of user locations and transaction parties in order to determine where DST applies.

Example Calculation

Here’s how a fictional marketplace with C$30 million Canadian digital revenue would calculate DST:

- Global revenue: €900 million (exceeds €750 million threshold)

- Canadian marketplace revenue: C$30 million (exceeds C$20 million threshold)

DST calculation:

- Total Canadian digital revenue: C$30 million

- Less deduction: C$20 million

- Taxable amount: C$10 million

- DST owed (3%): C$300,000

Remember, this C$300,000 is on top of any GST/HST, corporate income tax, or other obligations. It's an additional cost of doing business with Canadian users.

DST Compliance Steps (Even with Repeal Pending)

Registration

If your Canadian digital revenue exceeds C$10 million, you must register with the CRA by January 31 of the following year. Registration is required even if you don't hit the C$20 million DST threshold. This lower registration threshold helps the CRA track businesses approaching DST liability.

Register online through the CRA's My Business Account portal. Note that international businesses without existing CRA accounts need to first obtain a business number, which can take several weeks.

Corporate groups with multiple entities can designate one entity to handle DST obligations for all Canadian group members, simplifying compliance for complex corporate structures.

Record-Keeping and Group Election

Maintaining detailed records is vital for DST compliance:

- Transaction-level data showing user locations

- Revenue categorization by DST service type

- Documentation supporting your sourcing methodology

- Calculations showing threshold monitoring

Corporate groups need to file a group election designating which entity handles DST compliance. This election must be filed within the first DST return. Choose wisely here, because changing it later requires CRA approval.

Keep records for at least six years after the relevant tax year, as the CRA can audit DST filings like any other tax return.

Filing and Remittance

Originally, DST returns were due June 30 each year, with payment due the same day. The CRA requires electronic filing using a specific JSON format.

While filing is currently paused, the technical requirements remain in place. Returns must include:

- Detailed revenue breakdowns by category

- User location analysis

- Deduction allocation across group entities

- Supporting calculations in CRA-prescribed format

Even with the pause, smart businesses are retaining this data. If DST returns to active status, you'll need historical information ready. Plus, similar reporting requirements exist in other countries with DST regimes.

How Canada Compares to Other DST Regimes

France

France pioneered the modern DST with its 3% tax starting in 2019. The French DST shares Canada's 3% rate but uses different thresholds: €750 million globally and €25 million in French revenue.

Unlike Canada's current pause, France has continued to collect DST while OECD negotiations proceed, generating over €1 billion annually.

France's DST covers similar service categories but includes additional provisions for digital interface services. Their calculation methodology has become a model for other countries implementing DST.

United Kingdom

The UK has a 2% DST rate. Their thresholds are £500 million in global revenue and £25 million in UK revenue.

The UK DST focuses on search engines, social media platforms, and online marketplaces, and excludes data sales. This narrower scope reflects the UK's attempt to target specific large platforms while avoiding broader economic impacts.

Britain has committed to removing DST once the OECD's Pillar One framework takes effect, but they're maintaining the tax while international negotiations continue.

India

India recently repealed its 2% equalization levy, which functioned similar to DST, in 2025. This tax applied to e-commerce transactions and digital advertising services provided by non-resident companies.

India's repeal came after reaching agreements through the OECD framework, suggesting a potential path forward for other countries. However, India retained the right to reinstate digital taxes if cross-border agreements fail to materialize.

The Indian experience shows how quickly digital tax regimes can change—another reason why automated compliance systems have become essential.

How Sphere Makes DST (and Global Digital Tax) Easy

Full Visibility and Threshold Alerts

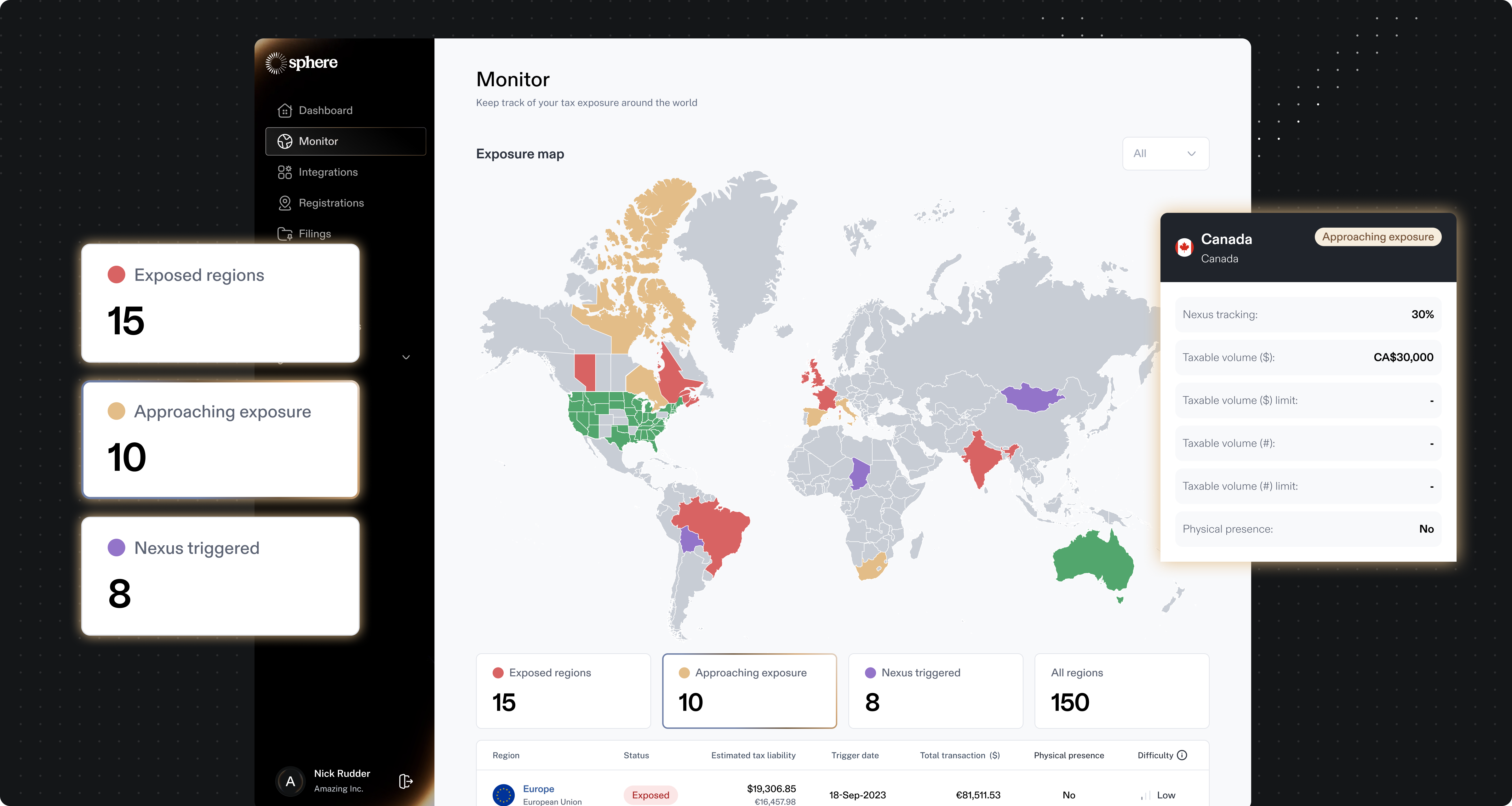

Sphere's AI-powered platform continuously monitors your revenue against DST thresholds in every country where these taxes exist. You'll know immediately when you're approaching registration or tax obligations, with no manual spreadsheet tracking needed.

The platform tracks both the global €750 million threshold and country-specific revenue thresholds simultaneously. Real-time alerts mean you're never surprised by new tax obligations, even as your business scales to new markets.

Sphere also monitors regulatory changes, updating threshold tracking as countries modify their DST rules.

Automated Tax Engine and Calculations

Sphere's proprietary Tax Review and Assessment Model (TRAM) uses AI to classify every transaction by revenue type and user location. The system automatically determines which revenues fall under DST categories and applies the correct sourcing rules for each country.

The platform handles complex attribution scenarios, like marketplace transactions with parties in multiple countries. Pro-rata calculations for group deductions happen automatically, with full audit trails showing how each number was determined.

Unlike manual calculations or basic tax software, Sphere's AI engine understands the nuances of each country's DST implementation. It knows that UK DST excludes financial services while French DST includes them, applying the right rules for each jurisdiction.

Streamlined Filing and Audit Trail

When DST filing requirements are active, Sphere generates fully compliant returns in each country's required format. For Canada, that means filings meeting all CRA specifications.

Every calculation, classification, and filing is documented with audit-ready records. If tax authorities question your DST treatment, you have comprehensive documentation showing exactly how you determined your obligations.

The platform also handles group elections and multi-entity filings, allowing for coordination of DST compliance across complex corporate structures without manual intervention.

Designed for Growing Finance Teams

Sphere charges a simple flat rate of $100 per month per jurisdiction. There are no usage fees, no overages, and no surprise bills as your company grows. Unlike legacy providers that charge based on transaction volume or revenue, Sphere's pricing stays predictable as you scale.

Implementation takes days, not months. The platform integrates with your existing billing and accounting systems through modern APIs, pulling transaction data automatically without manual uploads or reconciliation.

Companies like Runway, Replit, and ElevenLabs trust Sphere to handle their global tax complexity, freeing their finance teams to focus on strategic work instead of tax calculations.

The Current State of Canadian DST

Canada's DST situation perfectly illustrates why manual tax compliance no longer works for global digital businesses. Rules change quickly, requirements vary by country, and complexity keeps growing.

While the Canadian government has paused DST collection, the tax remains legally active and could return with little warning. Meanwhile, other countries continue expanding their digital tax regimes, creating an ever-more-complex compliance landscape.

Smart finance teams are preparing for this reality by implementing automated systems now. Whether DST returns to Canada or new digital taxes emerge elsewhere, you'll be ready with real-time tracking, accurate calculations, and compliant filings.

You Might Like

.png)

Make the world

one market

End-to-end compliance automation for sales tax, VAT, and GST. 100+ regions. One platform. Built by 50 people who believe the compliance cost of every transaction should be zero.